Business Start-Up Funding

Start-up Funding Options

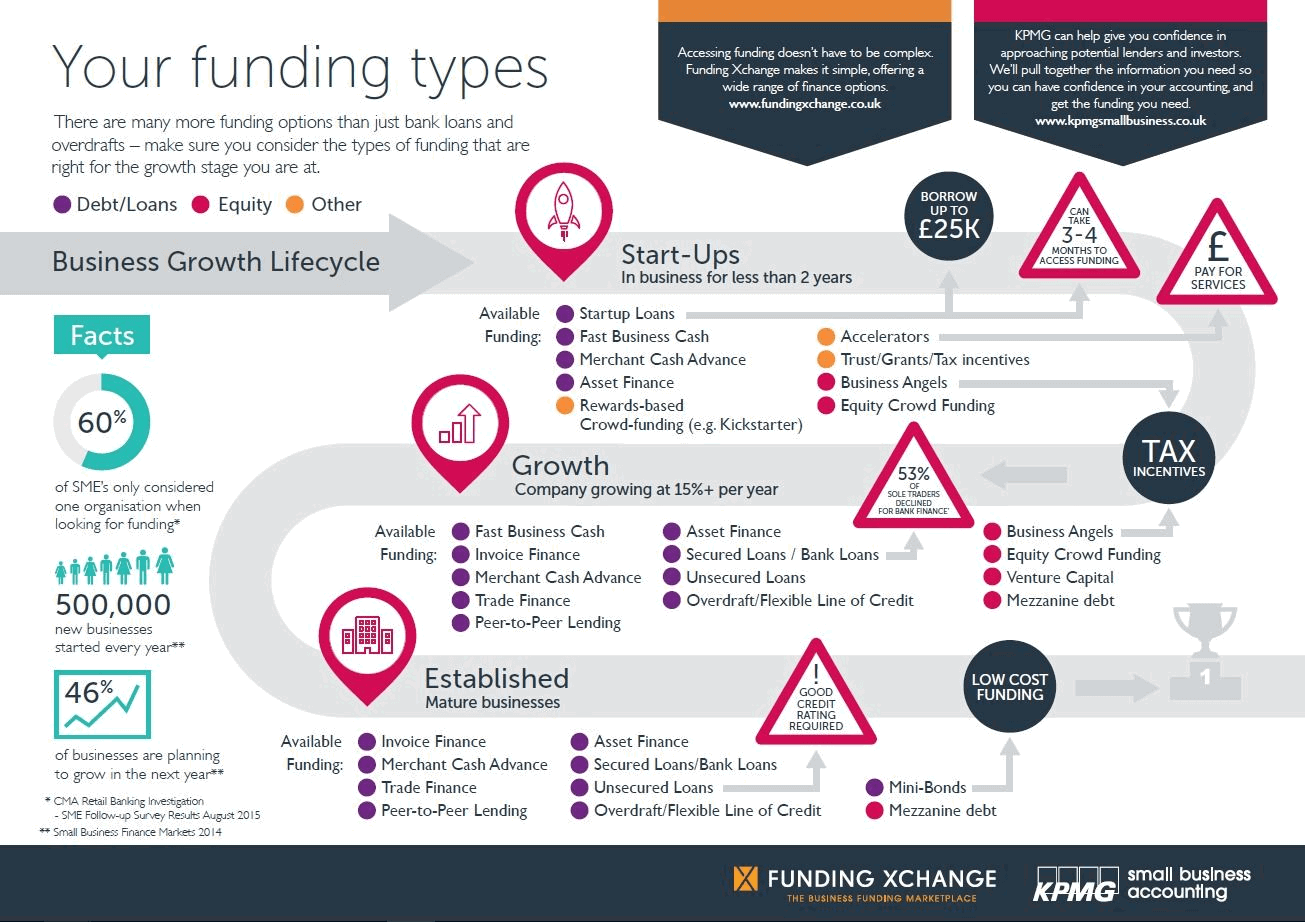

The options for obtaining finance for your start-up are numerous, as shown below in the Funding Xchange’s infographic.

Sourcing and securing finance is especially challenging while Coronavirus is wreaking havoc with the economy and it is likely to be more challenging than in more normal times. But that is no excuse for not assessing your needs and looking at the many available potential sources of finance.

So, this page covers some of the main sources of start-up finance and directs you to sites and other information aimed at giving you relevant and practical help when considering the type of finance that will be suitable for your new business.

The key message from Funding Xchange and others is to take time to consider the options and their implications. For example, it will be more costly (e.g. interest charges) to take a loan out than to sell shares in your company. But, selling shares means that you will reduce the amount of ownership that you have in your business.

There are always important differences and trade-offs to be looked at and weighed up between the types of finance. The legal documentation will also be different, depending on the route taken. A sale or new issue of shares in your start-up company will involve a different legal process and documents compared with taking out a loan.

Crowdfunding involves different processes again.

Some of the terminology that you are going to come across in your search for start-up finance can be confusing, so we have included a useful guide here from SeedLegals.com.

These and many other factors in start-up finance are covered in this help desk, which is designed to help you understand the landscape and give you a road map across it and provide you with a range of specially packaged legal templates to help you.

See also the Funding Xchange’s SME Funding Guide Part- 1.

Start-up financing is also supported and encouraged via the Government’s Seed Enterprise Investment Scheme, which gives tax benefits to businesses who qualify for the scheme and comply with its terms- see details below.

See also our blogs on Crowdfunding / Private Equity / Venture Capital

A start-up loan is going to be more risky for the lender than a loan made to a business that has been trading for a longer period. This means that the loans can be more expensive and may involve the entrepreneur giving some form of security for the repayment of the loan, which might be a personal guarantee or security over an asset, like a house.

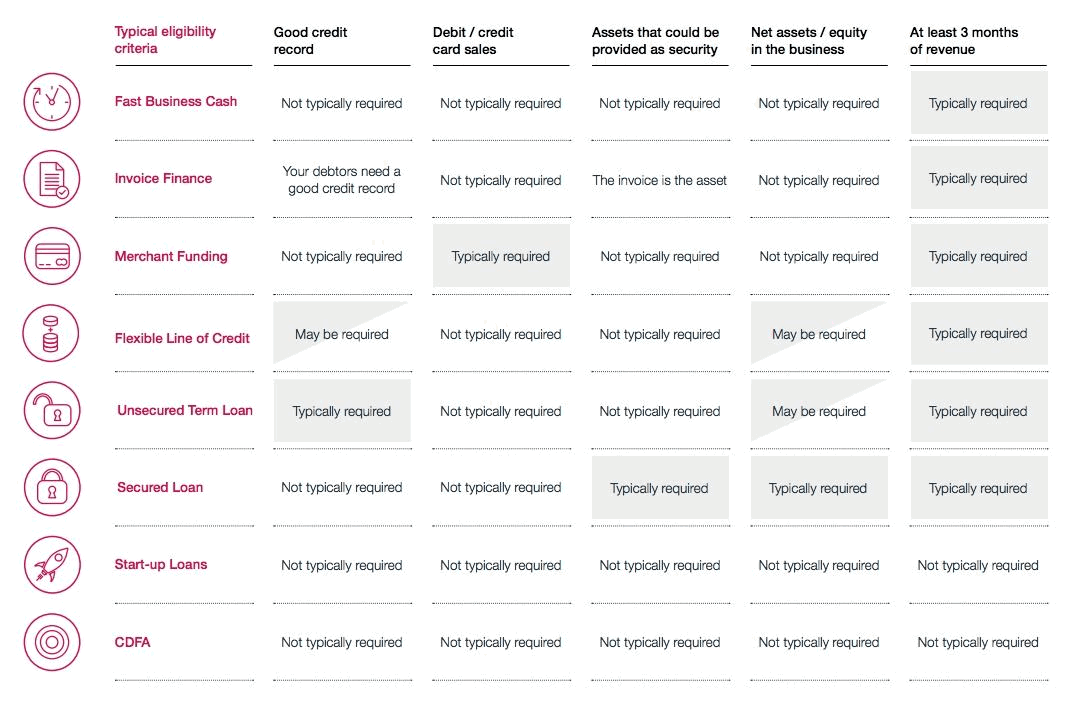

Start up loans can be obtained in a variety of ways shown in the table below from the Funding Xchange:

For start-ups, it is likely that a bank will require loan security in the form a personal guarantee from the founder(s), unless there are some tangible assets that can be secured, such as house or building that does not already have a loan secured on it, or other assets such as stock.

For more information on these type of loans, see this from startups.co.uk.

For comparison on different types of business loans, see this on money.co.uk.

Government–backed Loans

To apply for a Government backed start-up loan of £500 to £25,000 all of the following must apply:

- you live in the UK

- you’re 18 or over

- you have (or plan to start) a UK-based business that’s been fully trading for less than 24 months

Start-up Loans is a subsidiary of the British Business Bank and delivers the Government’s Start Up Loans programme providing finance and support for businesses who struggle to access other forms of finance.

Check if you are eligible for a start-up loan

Start up loan repayment calculator

For more information on these type of loans, including the application process, see this from startups.co.uk.

These are likely to be the cheapest and easiest loans to arrange at the early stages of a new business. They avoid some of the formalities of applying to a bank and they can often be organised more quickly. How much is borrowed and the level of ‘due diligence’ done by the friend or family member depends on a number of factors, such as how much they already know about the business.

SeedLegals.com provides helpful guidance on raising money from friends & family or from ‘someone you just met‘ and explains the different types of investor you may come across on your journey to find the right start-up finance for your business.

NetlawMan also offers some useful tips on what to do in arranging this type of loan and a template loan agreement.as well as the following in relation to organsing such a loan:

“Lending money – what you should record in an agreement

If ever there was a contract which should be put into writing it is a contract to lend money. Nothing provides a more fruitful source of disagreement (except perhaps religion!)

The circumstances of common transactions vary widely. Usually, an agreement is put in place by the lender, since it is his or her capital at risk, so this article considers what should be important to him or her.

Formal lending that a bank might undertake, such as a normal house mortgage or a corporate bond is outside the scope of this article.

Looking at less formal transactions, you might wish to lend to:

- your child, to buy a house

- a friend to engage in a new business, or get him out of personal financial trouble

- a business colleague in a business you jointly operate (such as lending him capital for his joint investment in the business)

- someone you know less well, for a good return on your money

We cannot emphasise enough how important it is to record the amount and terms of any loan in a written agreement.

If your borrower is someone you don’t know well, who offers you a good rate of interest for an amount that is otherwise sitting in a bank account not earning interest, you need to set down every possible consideration, so that you have confidence that you really are “agreed” on possible point.

If you are lending to someone you know very well – perhaps a friend or even one of your children, then it is just important to record the terms in writing. If you don’t, you can be sure that, between you, you will fail to consider some important element, upon which later you will find you have different views – and that is before you even begin to consider the terms where you have different recollections. The reason to have a written record might be to keep your relationship strong rather than to be a document that you want to enforce.

What your agreement should consider

The agreement you choose (or rather the terms that you include in it) will depend on:

- how far you trust the borrower to repay on time

- what confidence you have in the ability of the borrower to repay

- how you assess the chances of change for the worse in the affairs of the borrower

- how important it is to you to be repaid in specific terms – or at all

- how important it is to you to obtain the best rate of interest

Whether your loan is to someone close to home or at arm’s length, the main terms to consider are:

- how much money does the borrower require, and will this be enough to satisfy his or her full requirement for why he or she needs the money

- at what rate of interest and upon what other terms are you prepared to lend

- what information do you want up front, to satisfy yourself, or your business partners that the proposition is viable

- what security or third party guarantee can be provided and how tight do you want to make it

- what information do you require from time to time to stay satisfied that the borrower is solvent and that you will be first in line when the time for repayment arrives

- what will happen, in detail, if the borrower is unable to repay

Security

The question of security is worth deeper consideration. The three most common forms of security, in order of preference, are:

- traceable securities (such as public company shares) or intellectual property that can be sold

- a promise by a third party to pay or make good if the debtor fails – a personal guarantee

- goods given in security – usually plant or machinery that is difficult to move

Of course, most borrowers are not in a position to offer you the perfect security. If they were, they would probably be borrowing from a bank and not from you or your company. The main criteria to take into account in choosing security (if you have a choice) are:

- value in an open market sale

- liquidity – the ease with which they can be sold

- value to the borrower

Value

Obviously, security does not “secure” your cash loan unless the value you would receive on selling it is at least equal to the amount lent, plus accumulated interest and expenses.

Of course, you could imitate the position taken by a bank and ask for a “fixed and floating” charge. You would not take such a charge from an individual because it amounts to a personal guarantee, which is far easier to document and subsequently claim. But if the borrower is a company then an “F&F” gives you all the security you can obtain. What it amounts to is a charge on all the assets of the borrower, whether they are fixed assets such as cars or plant or office furniture, or floating assets which change constantly such as stock for sale of materials for manufacture.

We do not recommend a floating charge for use by individuals or small company lenders because there may be difficulties in proving ownership and right to sell. We recommend that you stay with specific assets that are easy to sell. If you must have floating assets, you should choose goods that are identifiable and that do not turn over too often, such as beef cows, rather than nuts and bolts.

Liquidity

Liquidity means not merely how easy it is to sell, but all things in connection with the sale.

Most lenders fail to assess the difficulties in liquidation certain types of security.

Ask yourself how you would go about selling a potato cleaning and sorting plant and how long it would take to make the sale.Compare that with a share transfer form (and certificate) for the sale of 100,000 shares in a FTSE 100 company.

There is a tendency for a borrower to offer as security the goods he intends to buy with the loan. This may seem neat, but it is not logical. If the borrower has better security, we recommend that you ask for it.

Value to the borrower

It is best to take security that is also of great value to the borrower. You may be able to sell security assets for only a small sum, but if they are worth far more to the borrower, then his effort to repay the loan will be correspondingly greater.

Lending to a close relative

Your money is at risk any time you fail to provide a proper agreement with appropriate safeguards. If you do not wish to tie down the borrower (for any reason) then you increase your risk.

Real property (buildings and land) as security

Real property is not as liquid as many financial assets, but certainly better than fixed plant. Such a security is of course usually called a mortgage or charge.

Taking title deeds as security

Before country wide land registration, real property could be taken as security by physical possession of the title deeds, without which the borrower could not deal with the property in any way, and which could form the basis of an application to court for the lender to sell the property. Today, that does not work.

To take a land certificate as informal security is a non-starter, for technical reasons we shall not here explain.

What about promissory notes?

Historically, a promissory note was useful as a means of recording money debts between people who trusted each other to pay.

Cheques now perform that function more efficiently.

The main problem with promissory notes today is that it is far easier than it was 200 years ago for the debtor to persuade a court that he has a good reason not to honour the note. In other words, the note may not tell the full and up-to-date story of the financial relationship.” Netlawman.co.uk.

“An angel investor is usually a high net worth individual who provides financial backing for small startups or entrepreneurs. Often, angel investors are found among an entrepreneur’s family and friends. The funds that angel investors provide may be a one-time investment to help the business get off the ground or an ongoing injection to support and carry the company through its difficult early stages.” Investopedia.com

“Angel investing is the most significant source of investment in startup and early-stage businesses seeking equity to grow their business.” UK Business Angels Association

There is a lot of practical information on the UK Business Angels Association for both sides of the investment equation: the entrepreneur and the angel investor.

Finding an angel investor for your type of business start-up.

A business grant is not a loan and nor is it an equity investment. Grants are usually publicly-funded schemes that offer cash awards, free equipment and tools and/or reduced costs for using vital resources.

Grants can be obtained from a number of sources for a variety of business start-ups. Grants may become repayable in some circumstances, for example if the grantee (recipient of the money) does not abide by its terms.

Useful list and information on the grants that are available can be found in the EntrepreneurHandbook.co.uk and at Startup.co.uk.

It is worth doing a lot of research into the types and scope of grant that are available to see if your start-up business might qualify for one. It could be the cheapest form of financing that you will find. Be aware that there are always terms and conditons attached to grants and these need to be carefully considered as well.

Raising money by asking a wide range of people to each contribute a relatively small amount of money. It is commonly done via online platforms set up specifically to connect with potential funders- see the blog on Crowdfunding.

This is money being placed into the start-up business through buying shares in a company that has been formed to run it.

Shares are issued to an investor, usually in return for cash, but also for in-kind contributions that have an agreed value. Examples of in-kind contributions are intellectual property like a computer programme, stock-in-trade, or services.

Equity start-up funding is likely to be cheaper than loans, as it usually will not involve the company paying any interest to the investor, who will be relying on receiving dividends from future profits and a capital return on his equity investment when he/she eventually sells the shares as and when the business succeeds.

The investor will, more often than not, take a minority stake in the company- commonly up to 30-35%, but it can occasionally be more- and will be providing much useful initial funding to help get the business under way.

Investors can come from a variety of places including the founding entrepreneur(s), friends & family and/or angel investors. Share (equity) can be issued with different rights for different shareholders.

For start-ups, it is usual to enter into a Shareholders’ Agreement to set out the rights and obligations of all of the investors.

Invoice Financing (factoring & discounting)

Assuming that your start-up has got to the stage of issuing invoices, it is possible to use your business debtors as a means of financing.

Usually, invoices are paid well after they are sent out to customers and clients, which means that the business can wait to get paid for as much as a month or more, in some cases. Cash starvation can easily and quickly cause serious problems and even bring a new business down.

Invoice financing allows a start-up (as well as more mature businesses) to accelerate getting paid, with important cash flow benefits.

Invoice financing can be arranged in a number of ways, most commonly by ‘factoring’ or ‘discounting’.

With factoring, the business sells its unpaid invoices to a lender, who might pay 70% to 85% of the invoice value more or less immediately, which means the business gets cash much more quickly than if it waited for its customers to pay.

Assuming the lender then receives full payment for the invoices, it will pay the remaining 15% to 30% of the invoice value to the business, less interest and/or fees charged for the service. Customers will be made aware of the factoring arrangement.

Alternatively, invoice discounting involves the business itself, not a lender, receiving invoices payments, so customers are not aware of any funding facility at work. A lender lends the business up to 95% of the invoice value and when customers pay their invoices, the business repays the lender, together with a fee or interest for making the loan.

The essential differences between factoring and discounting explained by FundingOptions.com

Some of the advantages and disadvantages of invoice financing from Startups.co.uk:

- Improved cash flow

- Quick purchasing

- Rapid expansion

- Improvement

- Debt protection

- Cost-effective admin

- Cost-effective debt collection

- Peace of mind

- Finance options

How to find and obtain invoice financing for your start-up- try these comparison website:

Seed Enterprise Investment Scheme (SEIS)

SEIS was first raised in Parliament in 2011, as start-ups were identified as important to the UK’s economic recovery. It was then implemented officially in April 2012.

SEIS is designed to help your company raise money when it’s starting to trade. It does this by offering tax reliefs to individual investors who buy new shares in your company.

You can receive a maximum of £150,000 through SEIS investments. This will:

- include any other de minimis state aid received in the 3 years up to and including the date of the investment

- count towards any limits for later investments through other venture capital schemes

There are various rules you must follow so your investors can claim and keep SEIS tax reliefs relating to their shares.

Tax reliefs will be withheld, or withdrawn, from your investors if you do not follow the rules for at least 3 years after the investment is made.

- How the scheme works

- Companies that can use the scheme

- About the investment

- Before raising your money

- How to apply

It is estimated that nearly 2,400 businesses have raised a total of about £190m using the SEIS in 2017 & 2018- HMRC’s May 2019 Report

For help with getting investments for your business start-up that are SEIS compliant try- SeedLegals.com

By the publications team at: Contracts-Direct.com with the assistance of the referenced third parties

Publisher: Atkins-Shield Ltd: Company No. 11638521

Registered Office: 71-75, Shelton Street, Covent Garden, London, WC2H 9JQ

Note: This publication does not necessarily deal with every important topic nor cover every aspect of the topics with which it deals. It is not designed to provide legal or other advice. The information contained in this document is intended to be for informational purposes and general interest only.

E&OE

Atkins-Shield Ltd © 2020